Last month, Delaware Call reported on proposed amendments to the state’s corporate code that would have upended more than a century of contract law in ways that would have greatly benefited the most powerful corporations and private equity firms in the country at the expense of everyone else.

Those proposed amendments were initially approved by a special committee within the Delaware State Bar Association (DSBA) in early April but were suddenly and without explanation pulled from final consideration after facing intense scrutiny by legal experts who said the changes would have allowed corporate interests to use stockholder agreements to circumvent the most important regulations ensuring transparency and accountability under Delaware corporate law’s board-centric regime.

Now, after weeks of silence, the DSBA has quickly approved newly revised proposed amendments to the corporate code and sent them to the General Assembly for approval by state legislators, who rarely debate or comment on the merits of amendments to the corporate code.

The amendments passed the DSBA Executive Committee last Thursday with two votes against. Minus three abstentions, the remaining members of the Executive Committee voted to approve, sending the amendments to the state Senate Judiciary Committee for consideration as Senate Bill 313. The bill is sponsored by Senate Majority Leader Bryan Townsend, with eight additional sponsors in the Senate and nine in the House.

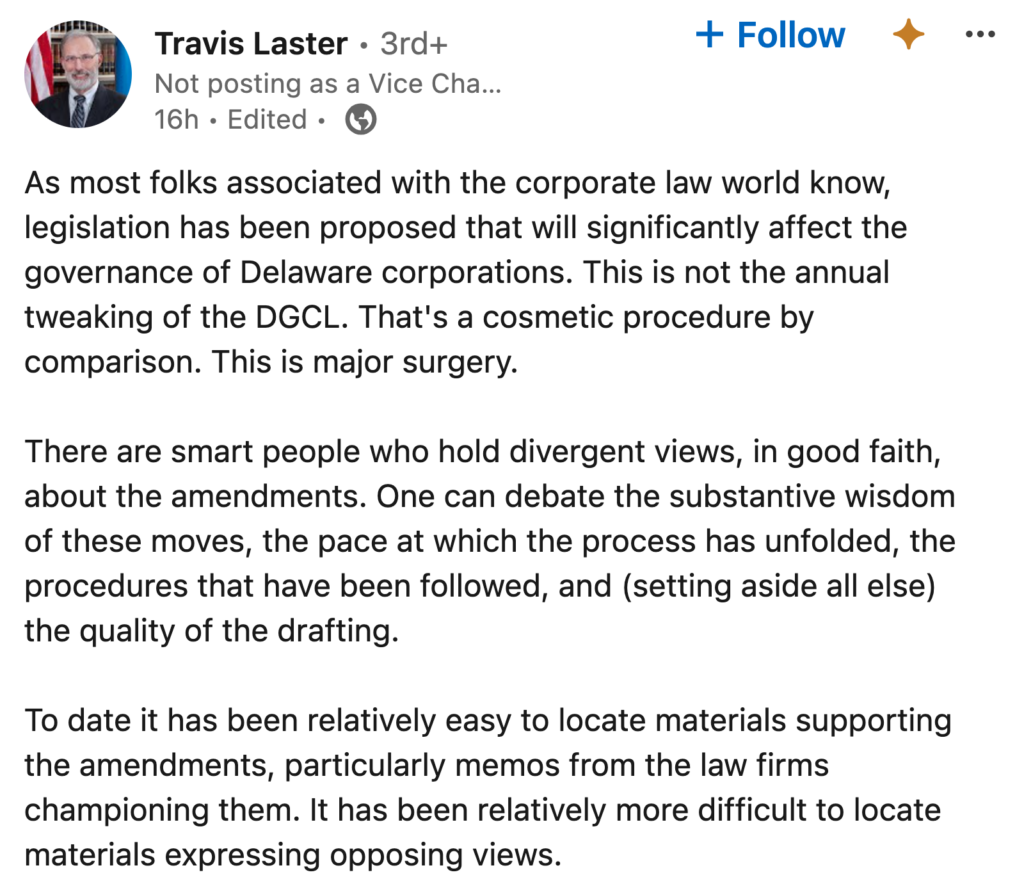

As Vice Chancellor Laster said late yesterday in a post on LinkedIn, the proposed amendments will “significantly affect the governance of Delaware corporations. This is not the annual tweaking of the [Delaware General Corporation Law]. That’s a cosmetic procedure by comparison. This is major surgery.”

While some law firms have suggested that the revised amendments are necessary to bring Delaware’s corporate law “in line with market practice,” doubts remain about the extent to which these amendments actually solve real problems or just benefit a handful of powerful private equity firms that have already entered into governance contracts that are illegal under existing law but would be retroactively legalized by the amendments. UCLA Law distinguished professor Stephen Bainbridge — author of hundreds of law review articles and one of the most widely cited scholars on corporate law — called for the amendments to be scrapped entirely.

“Memo to the Delaware corporate law council: the proposed amendments to the [Delaware General Corporation Law]. . . is one of the worst examples of statutory drafting I’ve ever seen,” Bainbridge posted on May 10 to the social media platform X, formerly known as Twitter. “It’s a complete mess. It’s hard to parse just from a grammatical standpoint and difficult to apply in a legal sense. Start over.”

How are the new corporate law amendments different?

Within Senate Bill 313 are three major changes to the corporate code that, if passed, will effectively overturn recent decisions handed down by the Delaware Court of Chancery, the venue for legal disputes between business entities incorporated in Delaware. One of those decisions, West Palm Beach Firefighters’ Pension Fund v. Moelis & Co., invalidated provisions of a stockholder agreement between the investment bank Moelis & Co. and its founder and chief executive officer that required his personal approval for nearly all consequential corporate decisions, including who would be allowed to sit on the board of directors.

The Court’s decision in Moelis, written by Vice Chancellor Laster, proved something of an unwelcome surprise to corporate interests, which had enacted thousands of these agreements over the past two decades. At risk of having these agreements declared facially invalid after the Moelis ruling, corporate interests moved quickly through proxies in the DSBA to put forward amendments to the Delaware corporate code that would essentially legalize what had just been struck down by the Court.

Vague wording in the earliest versions of the amendments appeared to leave open the possibility that agreements between corporations and influential shareholders, including private equity firms, could establish powers that supersede the authority of boards of directors and that are not spelled out in the certificate of incorporation. As Yale University law professor Sarath Sanga said to Delaware Call back in April, the lack of any guardrails in the original bill seemed to, among other things, “enable a board to cede, or a corporation to cede, 100 percent of its powers to an entity,” which would violate Delaware law because only natural persons are allowed to serve on boards of directors, who are to serve as the ultimate fiduciaries of the corporation. Could an LLC take the place of directors?

“This is something that has never been contemplated,” Sanga said.

That’s not all. According to critics, the previous version of the bill would have opened numerous other unusual loopholes in Delaware law, potentially changing corporate America as we know it by allowing publicly-traded companies to enter into all sorts of agreements with stockholders that could effectively be kept secret from the general public, or even other investors.

In other words, special interests would have had even more tools at their disposal to legally manipulate all sorts of corporate decisions, the impacts of which would be felt by everyone.

These newly revised amendments pull back on some of the more controversial changes to the corporate code from early April. Specifically, new language in the proposed bill specifies that no agreement “shall be enforceable against the corporation to the extent such contract provision is contrary to the certificate of incorporation or would be contrary to the laws of this State . . . if included in the certificate of incorporation.”

The new language also removed a phrase that would have allowed stockholder agreements to allow corporations to take actions that would otherwise “require approval of the board of directors,” which was criticized as a potential loophole around a key aspects of corporate governance — that directors are the ultimate fiduciaries of a company and must be the ones in charge.

Despite these and other revisions limiting the scope of stockholder agreements, however, some legal experts are still skeptical. Among the votes against the amendments on the DSBA Executive Committee was Secretary Mae Oberste, who cautioned against moving too quickly on amendments that could have such profound ramifications.

“I remain disappointed in the rushed process by which these proposed amendments have made their way to the General Assembly and wish there had been more opportunities for others to offer their input to the Council,” she said in a statement to Delaware Call. “Nonetheless, I am confident, should the amendments be enacted, that the Delaware judiciary will exercise its expertise to even-handedly apply the law and equitable principles.”

In a letter sent to the DSBA Executive Committee while it was still deliberating the amendments, the nonprofit Council of Institutional Investors urged the committee to shelve the measures, in part because they appeared to be responding to court rulings that had not yet worked their way through the appeals process, including the Moelis case.

“Although our concerns relate to the substance of the legislative proposals, the more pressing concern is the pace at which legislation is being proposed to overturn a single trial court ruling that is not yet even final,” the Council wrote. “We urge the Delaware State Bar Association to pause the process to permit a more complete consideration of the critical issues raised by the proposed legislation and their potential impact on long-term institutional investors.”

Some law professors are equally skeptical.

In an interview with Delaware Call, University of Michigan professor Gabriel Rauterberg said that the current version of the bill is not what he “would have drafted,” in part because the language still allows directors to enter into contracts without approval from shareholders.

“We think it would be preferable if the proposed amendment had required majority approval by a stockholder vote to adopt such a contract,” Rauterberg said on behalf of himself and his research partner, Yale Law professor Sarath Sanga. “We would have required such a vote, or pre-approval in the charter of such provisions, before corporations could enter these contracts. The new proposal still considerably expands the board’s ability to give away its power.”

These concerns are shared by Harvard Law professor Lucian A. Bebchuk, who called the revised amendments “especially problematic,” in an article posted to the Harvard Law School Forum on Corporate Governance:

There are good reasons for the long-standing corporate law rules that require advance notice and approval by a majority of outstanding shares for changes in the corporate charter. And these good reasons imply that it is undesirable to enable private parties to practically circumvent these safeguards. For any given opt-out corporations are allowed to effect via a charter change, I do not see any good reason, and supporters of the proposed legislation have not advanced such a reason, for facilitating a way around the notice and stockholder approval requirements.

“Further muddying the waters is this,” wrote law professor Ann Lipton on her blog. “The new amendments say that stockholder contracts can’t go beyond what a charter amendment would permit except with respect to DGCL §115, which . . . requires that a Delaware forum be available for claims.”

Instead of legal cases being heard in Delaware courts, the bill stipulates that stockholder agreements may require disputes be resolved in arbitration “to adjudicate claims under the contracts,” according to the synopsis. In other words, if shareholders decide to challenge the terms of a stockholder agreement a corporation entered into without their knowledge, the case may be forced into private arbitration and their complaints never be made public.

Furthermore, although the revised amendments pull back on language that would have allowed stockholder agreements to bypass boards of directors, NYU professors Marcel Kahan and Edward Rock recently suggested that even the revised amendments still leave too much uncertainty when it comes to the governing authority of directors.

If the proposed amendments are adopted, they write, there will no longer be “meaningful limits on a board’s ability to delegate key governance functions and responsibilities.”

How badly do these amendments undermine traditional governing structures within a corporation? Vice Chancellor Laster suggested in an earlier LinkedIn post that the amendments would seem to authorize a corporation entering into an agreement in which the “corporation [was] constrained to adhere to what [an] AI decided” and that “if Section 122(18) is enacted . . . a framework for bringing AI into the boardroom will exist under Delaware law.”

Still others are asking: Why now? Especially when the Moelis case has yet to work its way through the appeals process. Anat Alon-Beck, associate professor of law at Case Western Reserve University, said in an email to Law360 there was no need to change the law and that the Moelis case should proceed to the state’s Supreme Court. Professors Kahan and Rock agree: “The Delaware General Assembly should hold off until after the Delaware Supreme Court has had an opportunity to address these issues.”

Lastly, Chancellor Kathaleen McCormick also submitted a letter to the DSBA Executive Committee regarding the proposed amendments to the corporate code; however, the contents of that letter have not yet been made public.

“Wherever this ends up, it seems likely that a generation of corporate law professors will be able to get tenure based on research agendas tied to the legislation,” Vice Chancellor Laster concluded in his latest LinkedIn post. “The amendments raise deep questions about corporate theory and legal doctrine. They invite updated assessments of Delaware’s political economy and the mechanisms used to update the DGCL. They will likely produce myriad natural experiments for quantitative analysis. History is unfolding in real time. Enjoy!”